Back to Parish & Company Home Page

Monday, May 15, 2000 6:00 am Eastern Time

Company Press Release - Subject of Jeff Rense Interview on May 23, 2000

SOURCE: Parish & Company © Copyright

All Rights Reserved

Dell Financial Practices Lead to "Watered Stock"

PORTLAND, Ore., May 15 -- Dell Computer is a great company

that has pioneered the development of a direct sales model using the Internet.

Thus far stockholders have been richly rewarded. At the same time,

however, a remarkable deterioration in the quality of Dell's financial

condition has gone largely unnoticed.

Unlike Microsoft, Cisco Systems and Intel, Dell is primarily

an assembler of other products and is therefore limited in the margins

it can earn in a progressively more competitive environment. For

Dell, total revenue increases are not nearly as important as increases

in total gross margin dollars. What also makes Dell unique compared to

these other companies is the extent to which Michael Dell is rewarding

himself.

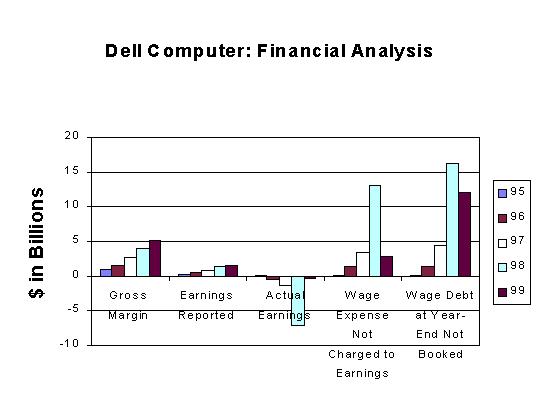

The following chart summarizes Dell's key financial results

based upon reports filed with the Securities and Exchange Commission.

The stock price used to reflect the wage debt for the fiscal year 1999

ending January 31, 2000 is the price on May 12, 2000. This was done

to make the analysis current. Although fiscal 1999 looks better in

terms of wage debt outstanding not booked at year-end, because the stock

price remained flat, the company's wage expense not charged to earnings

actually accelerated as outlined in the text following the chart.

Even though Dell's gross margin dollars are increasing,

this increase is being more than offset by the granting of excessive employee

stock options that has placed investors in a mathematical vice. With

320 million shares now owed to employees, this wage debt increases $320

million for every one dollar increase in Dell's stock price. A mere

$5 increase would erase there entire reported net income for the most recent

year. More significant, however, is that Dell now has 3 billion shares

outstanding, including the employee stock options. The entire gross

margin for the most current year is therefore equivalent to a $2 change

in the stock price. Dell has clearly become a "watered stock."

What few investors realize is that, based upon a review

of Dell's SEC filings for the fiscal year 1999 ending on January 28, 2000,

the company took a tax deduction for wages on its tax return for options

exercised and retired in excess of $3 billion, not a dime of which is charged

to the publicly disclosed earnings we see. Earnings are therefore

a mirage as Dell has effectively removed its biggest cost of doing business

from the earnings statement via a legal accounting loophole.

This wage expense deduction has also allowed the company

to eliminate its federal income tax liability on current product sales,

conserving more than $1 billion in cash in the most recent year.

This is because this wage deduction for stock options exercised and retired

now exceeds the taxable income from product sales. Since employees

are taxed on options exercised as normal wage income, even if the stock

is not sold, the IRS correspondingly allows the company to take a tax deduction.

Most technology companies do not have adequate profits to fully utilize

this deduction yet Dell, with its large profits, can utilize most of the

deduction.

Completely independent of the options cashed in and retired

is a remaining wage debt in excess of $12 billion based upon the market

price of $49 on May 12, 2000. This is computed as the market price

of $49 less the average exercise price of $11.40 times the 320 million

remaining options owed outstanding. Investors are in a mathematical

vice because this liability increases $320 million for every $1 increase

in the stock price.

For the quarter just ended on 4/30/2000 Dell did post

impressive sales gains yet beneath the surface are other significant issues

that most investors cannot fully see. Again, what is critical

for Dell are gross margin dollars, not total revenues.

The first additional area of concern is that the $125

million of investment gains taken represents 20 percent of the entire operating

income. On Sunday the NY Times did a feature titled "Levitating Earnings,

An Act or a Fact" and highlighted companies that are meeting expectations

by selling investments. Strangely, Dell was not cited in the

article.

Another little understood unique risk to Dell not seen

at most other high technology firms is that the company is speculating

on its own stock in the options market, betting both that it won't go above

a certain price and also betting that it won't fall below a certain price.

These are two separate speculations. The company's assumption is that the

stock will trade within a certain range and that they will be able to pocket

cash from premiums paid by these investors when the options expire worthless.

The company justifies this activity by saying it is a

good way to generate cash to contribute to financing the needed stock buybacks

to reduce dilution from the effect of the employee stock option program.

If losses are incurred the company will cover such losses by simply issuing

more shares and by doing so not be required to reflect a liability on the

balance sheet nor a cost to the income statement for such losses.

Even more unusual is that while the company is aggressively

buying back stock, in part financed from taking high risk speculations

on its own stock in the options market, the founder, Michael Dell, is aggressively

selling stock according to a recent Barron's article. Mr. Dell has

sold more than $800 million in stock during the 6 months ended March 31,

2000 while the company has repurchased more than $500 million in the 3

months ending April 30th.

Mr. Dell also received a significant grant of new options

during the same year. An obvious question for him might be, aren't your

massive stock holdings incentive enough to perform well? As Newsweek

noted in a November 1999 story titled "Clean Up Time, Is any useful corporate

purpose served by heaping options on top of already massive stock holdings-what

Wall Street calls piling pig on pork?"

The Dell Corporation is also issuing significant amounts of restricted

stock for various purposes, causing further dilution of existing shares,

as noted in its SEC filing available at www.edgar.gov.

Another important trend is that the company has doubled the amount of

sales for which it is providing financing, $1.8 billion for the most recent

year ended. This implies new risks, especially given Dell's focus

on high end Windows NT based web server products. Dell has been slow

to offer Linux based systems which now enjoy broad acceptance in this key

market and offer significant cost savings advantages to customers.

According to Yahoo, the largest holders of Dell stock are AXA Financial

Inc.which owns 126 million shares valued at more than $6.5 billion followed

by Barclays Bank Plc, Janus Capital Corporation, Fidelity Investments,

State Street, Vanguard, Taunus Corporation and Goldman Sachs.

Although Dell had a bright beginning, it has clearly compromised its

financial future due to the use of these financial practices, resulting

in a "watered stock." Parish & Company would strongly support

any efforts by the SEC to prohibit companies like Dell from conducting

stock buybacks while they are simultaneously engaging on speculations on

there own stock in the options markets.

Bill Parish, President of Parish & Company, has been quoted extensively

in a variety of major news publications, as well as The Tech Review, a

Canadian investment journal, Bild, the largest paper in Germany, The Fleet

Street Letter, a prestigious investment publication, The Spotlight, a conservative

newspaper and free market advocate and The Independent, a major British

newspaper. He has been interviewed by the New York Times, Infoworld, ZD

Net, Wall Street Journal, Newsweek and USA Today in addition to appearing

on ABC news and various radio stations including KUIK in Portland,

KIRO in Seattle and Aspen Public Radio in Colorado.

Mr. Parish is a Registered Investment Advisor and former CPA providing

fee based investment management services in addition to assisting companies

structure their 401k plans to meet their fiduciary obligations and provide

top quality well diversified investment choices at the lowest cost. Please

consider hiring Bill to be a permanent member of your 401K committee and

thereby utilize the services of a top investment professional in order

to clearly communicate your commitment to managing your employees 401K

plan or what can now be called there "Mutual Savings Bank."

Bill Parish

Parish & Company

10260 SW Greenburg Rd., Suite 400

Portland, OR 97223

Tel: 503-643-6999 Fax: 503-221-3161

email: bill@billparish.com

Back to Parish & Company Home Page